This function creates a chi-plot of given bivariate copula data.

BiCopChiPlot(u1, u2, PLOT = TRUE, mode = "NULL", ...)Arguments

- u1, u2

Data vectors of equal length with values in \([0,1]\).

- PLOT

Logical; whether the results are plotted. If

PLOT = FALSE, the valueslambda,chiandcontrol.boundsare returned (see below; default:PLOT = TRUE).- mode

Character; whether a general, lower or upper chi-plot is calculated. Possible values are

mode = "NULL","upper"and"lower"."NULL"= general chi-plot (default)"upper"= upper chi-plot"lower"= lower chi-plot- ...

Additional plot arguments.

Value

- lambda

Lambda-statistics (x-axis).

- chi

Chi-statistics (y-axis).

- control.bounds

A 2-dimensional vector of bounds \(((1.54/\sqrt{n},-1.54/\sqrt{n})\), where \(n\) is the length of

u1and where the chosen values correspond to an approximate significance level of \(10\%\).

Details

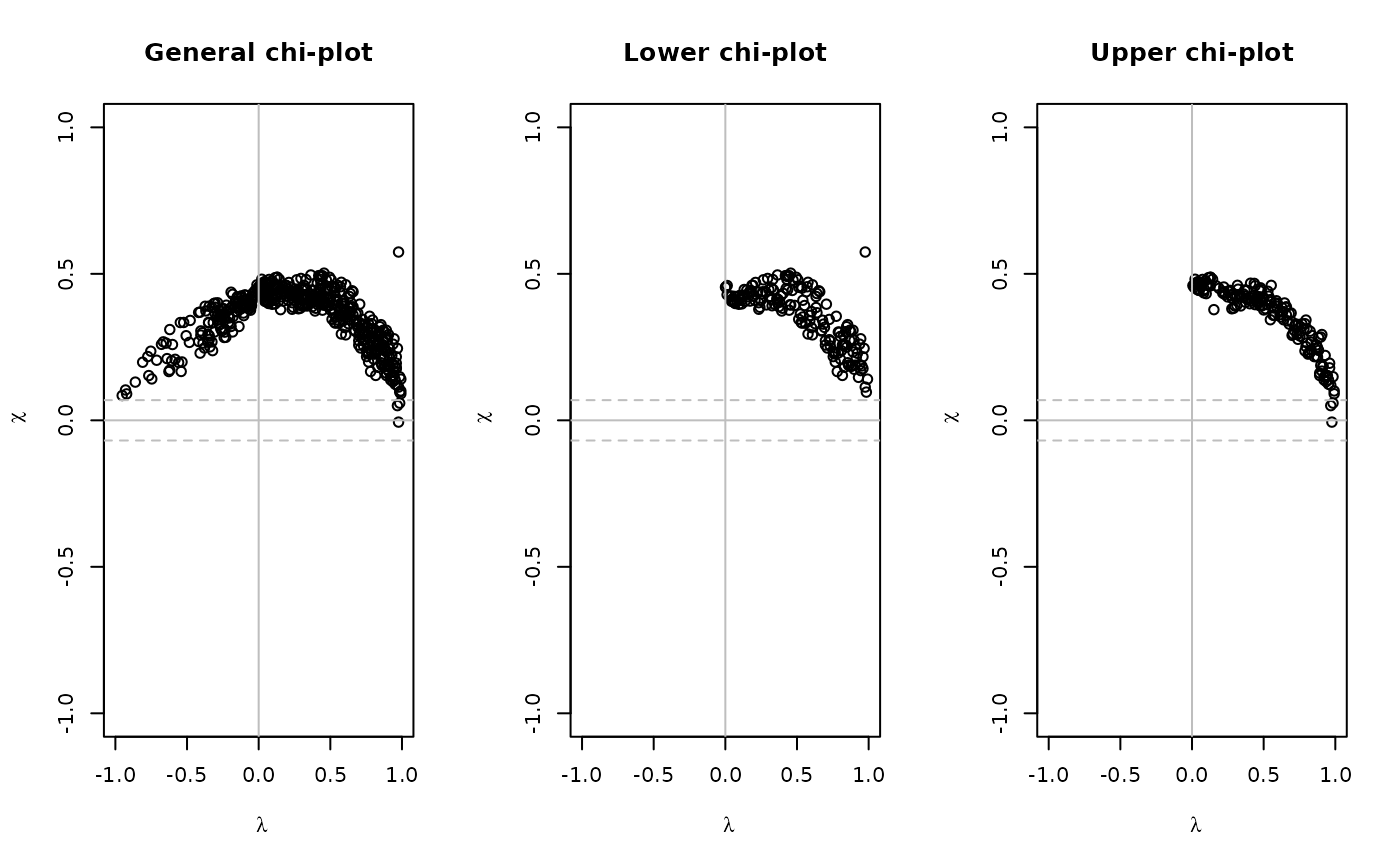

For observations \(u_{i,j},\ i=1,...,N,\ j=1,2,\) the chi-plot is based on the following two quantities: the chi-statistics $$\chi_i = \frac{\hat{F}_{1,2}(u_{i,1},u_{i,2}) - \hat{F}_{1}(u_{i,1})\hat{F}_{2}(u_{i,2})}{ \sqrt{\hat{F}_{1}(u_{i,1})(1-\hat{F}_{1}(u_{i,1})) \hat{F}_{2}(u_{i,2})(1-\hat{F}_{2}(u_{i,2}))}}, $$ and the lambda-statistics $$\lambda_i = 4 sgn\left( \tilde{F}_{1}(u_{i,1}),\tilde{F}_{2}(u_{i,2}) \right) \cdot \max\left( \tilde{F}_{1}(u_{i,1})^2,\tilde{F}_{2}(u_{i,2})^2 \right), $$ where \(\hat{F}_{1}\), \(\hat{F}_{2}\) and \(\hat{F}_{1,2}\) are the empirical distribution functions of the uniform random variables \(U_1\) and \(U_2\) and of \((U_1,U_2)\), respectively. Further, \(\tilde{F}_{1}=\hat{F}_{1}-0.5\) and \(\tilde{F}_{2}=\hat{F}_{2}-0.5\).

These quantities only depend on the ranks of the data and are scaled to the interval \([0,1]\). \(\lambda_i\) measures a distance of a data point \(\left(u_{i,1},u_{i,2}\right)\) to the center of the bivariate data set, while \(\chi_i\) corresponds to a correlation coefficient between dichotomized values of \(U_1\) and \(U_2\). Under independence it holds that \(\chi_i \sim \mathcal{N}(0,\frac{1}{N})\) and \(\lambda_i \sim \mathcal{U}[-1,1]\) asymptotically, i.e., values of \(\chi_i\) close to zero indicate independence—corresponding to \(F_{1, 2}=F_{1}F_{2}\).

When plotting these quantities, the pairs of \(\left(\lambda_i, \chi_i \right)\) will tend to be located above zero for positively dependent margins and vice versa for negatively dependent margins. Control bounds around zero indicate whether there is significant dependence present.

If mode = "lower" or "upper", the above quantities are

calculated only for those \(u_{i,1}\)'s and \(u_{i,2}\)'s which are

smaller/larger than the respective means of

u1\(=(u_{1,1},...,u_{N,1})\) and

u2\(=(u_{1,2},...,u_{N,2})\).

References

Abberger, K. (2004). A simple graphical method to explore tail-dependence in stock-return pairs. Discussion Paper, University of Konstanz, Germany.

Genest, C. and A. C. Favre (2007). Everything you always wanted to know about copula modeling but were afraid to ask. Journal of Hydrologic Engineering, 12 (4), 347-368.

See also

Examples

## chi-plots for bivariate Gaussian copula data

# simulate copula data

fam <- 1

tau <- 0.5

par <- BiCopTau2Par(fam, tau)

cop <- BiCop(fam, par)

set.seed(123)

dat <- BiCopSim(500, cop)

# create chi-plots

op <- par(mfrow = c(1, 3))

BiCopChiPlot(dat[,1], dat[,2], xlim = c(-1,1), ylim = c(-1,1),

main="General chi-plot")

BiCopChiPlot(dat[,1], dat[,2], mode = "lower", xlim = c(-1,1),

ylim = c(-1,1), main = "Lower chi-plot")

BiCopChiPlot(dat[,1], dat[,2], mode = "upper", xlim = c(-1,1),

ylim = c(-1,1), main = "Upper chi-plot")

par(op)

par(op)