This function creates a Kendall's plot (K-plot) of given bivariate copula data.

BiCopKPlot(u1, u2, PLOT = TRUE, ...)Arguments

Value

- W.in

W-statistics (x-axis).

- Hi.sort

H-statistics (y-axis).

Details

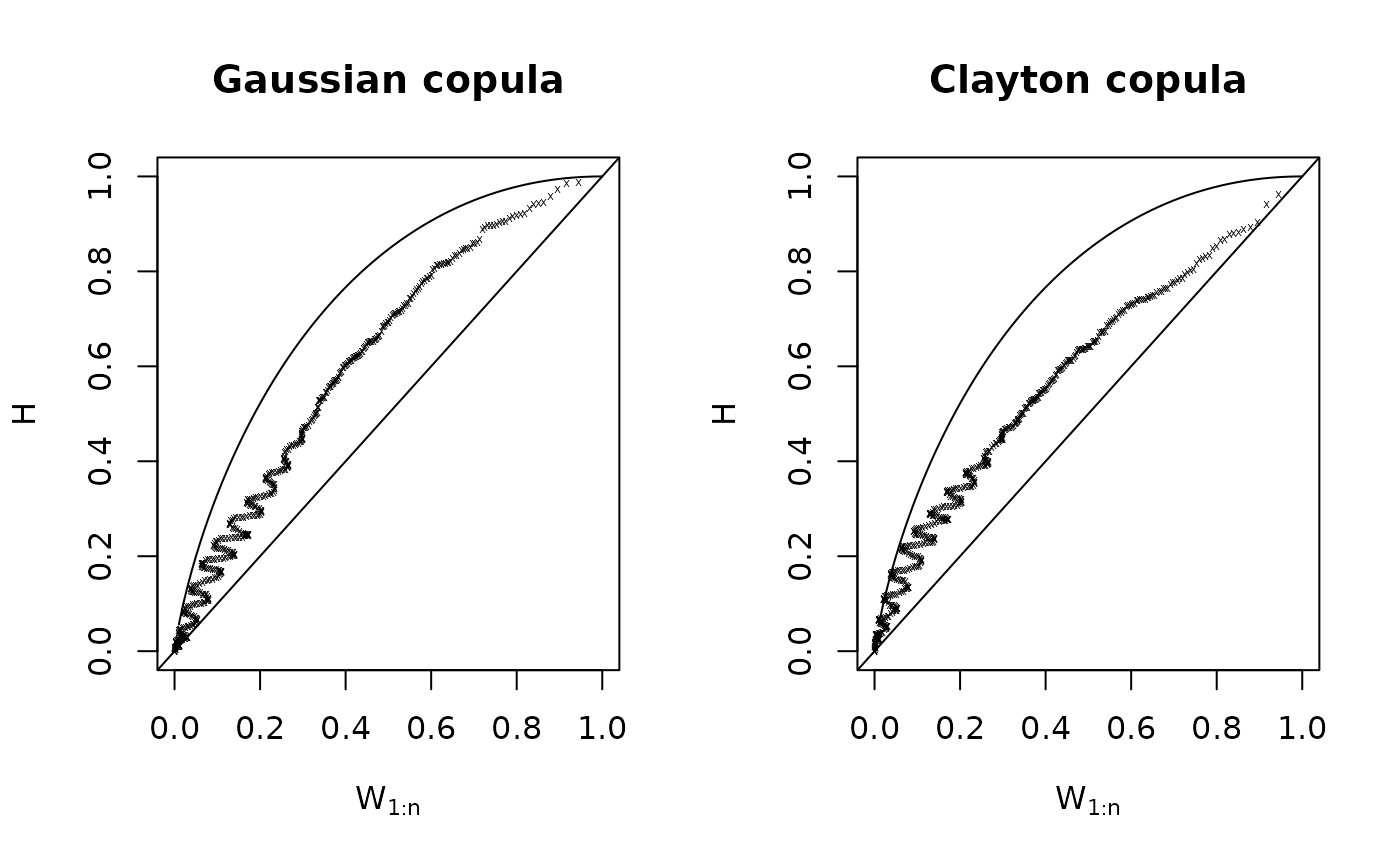

For observations \(u_{i,j},\ i=1,...,N,\ j=1,2,\) the K-plot considers two quantities: First, the ordered values of the empirical bivariate distribution function \(H_i:=\hat{F}_{U_1U_2}(u_{i,1},u_{i,2})\) and, second, \(W_{i:N}\), which are the expected values of the order statistics from a random sample of size \(N\) of the random variable \(W=C(U_1,U_2)\) under the null hypothesis of independence between \(U_1\) and \(U_2\). \(W_{i:N}\) can be calculated as follows $$ W_{i:n}= N {N-1 \choose i-1} \int\limits_{0}^1 \omega k_0(\omega) ( K_0(\omega) )^{i-1} ( 1-K_0(\omega) )^{N-i} d\omega, $$ where $$K_0(\omega) = \omega - \omega \log(\omega), $$ and \(k_0(\cdot)\) is the corresponding density.

K-plots can be seen as the bivariate copula equivalent to QQ-plots. If the points of a K-plot lie approximately on the diagonal \(y=x\), then \(U_1\) and \(U_2\) are approximately independent. Any deviation from the diagonal line points towards dependence. In case of positive dependence, the points of the K-plot should be located above the diagonal line, and vice versa for negative dependence. The larger the deviation from the diagonal, the stronger is the degree of dependency. There is a perfect positive dependence if points \(\left(W_{i:N},H_i\right)\) lie on the curve \(K_0(\omega)\) located above the main diagonal. If points \(\left(W_{i:N},H_i\right)\) however lie on the x-axis, this indicates a perfect negative dependence between \(U_1\) and \(U_2\).

References

Genest, C. and A. C. Favre (2007). Everything you always wanted to know about copula modeling but were afraid to ask. Journal of Hydrologic Engineering, 12 (4), 347-368.

See also

Examples

## Gaussian and Clayton copulas

n <- 500

tau <- 0.5

# simulate from Gaussian copula

fam <- 1

par <- BiCopTau2Par(fam, tau)

cop1 <- BiCop(fam, par)

set.seed(123)

dat1 <- BiCopSim(n, cop1)

# simulate from Clayton copula

fam <- 3

par <- BiCopTau2Par(fam, tau)

cop2 <- BiCop(fam, par)

set.seed(123)

dat2 <- BiCopSim(n, cop2)

# create K-plots

op <- par(mfrow = c(1, 2))

BiCopKPlot(dat1[,1], dat1[,2], main = "Gaussian copula")

BiCopKPlot(dat2[,1], dat2[,2], main = "Clayton copula")

par(op)

par(op)