Sequential Specification of R- and C-Vine Copula Models

Source:R/RVineStructureSelect.R

RVineStructureSelect.RdThis function fits either an R- or a C-vine copula model to a d-dimensional

copula data set. Tree structures are determined and appropriate pair-copula

families are selected using BiCopSelect() and estimated

sequentially (forward selection of trees).

RVineStructureSelect(

data,

familyset = NA,

type = 0,

selectioncrit = "AIC",

indeptest = FALSE,

level = 0.05,

trunclevel = NA,

progress = FALSE,

weights = NA,

treecrit = "tau",

rotations = TRUE,

se = FALSE,

presel = TRUE,

method = "mle",

cores = 1

)Arguments

- data

An N x d data matrix (with uniform margins).

- familyset

An integer vector of pair-copula families to select from. The vector has to include at least one pair-copula family that allows for positive and one that allows for negative dependence. Not listed copula families might be included to better handle limit cases. If

familyset = NA(default), selection among all possible families is performed. Coding of pair-copula families is the same as inBiCop().- type

Type of the vine model to be specified:

0or"RVine"= R-vine (default)1or"CVine"= C-vine

C- and D-vine copula models with pre-specified order can be specified usingCDVineCopSelectof the package CDVine. Similarly, R-vine copula models with pre-specified tree structure can be specified usingRVineCopSelect().- selectioncrit

Character indicating the criterion for pair-copula selection. Possible choices:

selectioncrit = "AIC"(default),"BIC", or"logLik"(seeBiCopSelect()).- indeptest

logical; whether a hypothesis test for the independence of

u1andu2is performed before bivariate copula selection (default:indeptest = FALSE; seeBiCopIndTest()). The independence copula is chosen for a (conditional) pair if the null hypothesis of independence cannot be rejected.- level

numeric; significance level of the independence test (default:

level = 0.05).- trunclevel

integer; level of truncation.

- progress

logical; whether the tree-wise specification progress is printed (default:

progress = FALSE).- weights

numeric; weights for each observation (optional).

- treecrit

edge weight for Dissman's structure selection algorithm, see Details.

- rotations

If

TRUE, all rotations of the families infamilysetare included.- se

Logical; whether standard errors are estimated (default:

se = FALSE).- presel

Logical; whether to exclude families before fitting based on symmetry properties of the data. Makes the selection about 30\ (on average), but may yield slightly worse results in few special cases.

- method

indicates the estimation method: either maximum likelihood estimation (

method = "mle"; default) or inversion of Kendall's tau (method = "itau"). Formethod = "itau"only one parameter families and the Student t copula can be used (family = 1,2,3,4,5,6,13,14,16,23,24,26,33,34or36). For the t-copula,par2is found by a crude profile likelihood optimization over the interval (2, 10].- cores

integer; if

cores > 1, estimation will be parallelized within each tree (usingparallel::parLapply()). Note that parallelization causes substantial overhead and may be slower than single-threaded computation when dimension, sample size, or family set are small ormethod = "itau".

Value

An RVineMatrix() object with the selected structure

(RVM$Matrix) and families (RVM$family) as well as sequentially

estimated parameters stored in RVM$par and RVM$par2. The object

is augmented by the following information about the fit:

- se, se2

standard errors for the parameter estimates; note that these are only approximate since they do not account for the sequential nature of the estimation,

- nobs

number of observations,

- logLik, pair.logLik

log likelihood (overall and pairwise)

- AIC, pair.AIC

Akaike's Informaton Criterion (overall and pairwise),

- BIC, pair.BIC

Bayesian's Informaton Criterion (overall and pairwise),

- emptau

matrix of empirical values of Kendall's tau,

- p.value.indeptest

matrix of p-values of the independence test.

Details

R-vine trees are selected using maximum spanning trees w.r.t. some edge weights. The most commonly used edge weight is the absolute value of the empirical Kendall's tau, say \(\hat{\tau}_{ij}\). Then, the following optimization problem is solved for each tree: $$\max \sum_{\mathrm{edges }\; e_{ij} \in \; \mathrm{ in \; spanning \; tree}} |\hat{\tau}_{ij}|, $$ where a spanning tree is a tree on all nodes. The setting of the first tree selection step is always a complete graph. For subsequent trees, the setting depends on the R-vine construction principles, in particular on the proximity condition.

Some commonly used edge weights are implemented:

"tau" | absolute value of empirical Kendall's tau. |

"rho" | absolute value of empirical Spearman's rho. |

"AIC" | Akaike information (multiplied by -1). |

"BIC" | Bayesian information criterion (multiplied by -1). |

"cAIC" | corrected Akaike information criterion (multiplied by -1). |

If the data contain NAs, the edge weights in "tau" and "rho" are

multiplied by the square root of the proportion of complete observations. This

penalizes pairs where less observations are used.

The criteria "AIC", "BIC", and "cAIC" require estimation and

model selection for all possible pairs. This is computationally expensive and

much slower than "tau" or "rho".

The user can also specify a custom function to calculate the edge weights.

The function has to be of type function(u1, u2, weights) ... and must

return a numeric value. The weights argument must exist, but does not has to

be used. For example, "tau" (without using weights) can be implemented

as follows:function(u1, u2, weights) abs(cor(u1, u2, method = "kendall", use = "complete.obs"))

The root nodes of C-vine trees are determined similarly by identifying the node with strongest dependencies to all other nodes. That is we take the node with maximum column sum in the empirical Kendall's tau matrix.

Note that a possible way to determine the order of the nodes in the D-vine is to identify a shortest Hamiltonian path in terms of weights \(1-|\hat{\tau_{ij}|}\). This can be established for example using the package TSP. Example code is shown below.

Note

For a comprehensive summary of the vine copula model, use

summary(object); to see all its contents, use str(object).

References

Brechmann, E. C., C. Czado, and K. Aas (2012). Truncated regular vines in high dimensions with applications to financial data. Canadian Journal of Statistics 40 (1), 68-85.

Dissmann, J. F., E. C. Brechmann, C. Czado, and D. Kurowicka (2013). Selecting and estimating regular vine copulae and application to financial returns. Computational Statistics & Data Analysis, 59 (1), 52-69.

Examples

# load data set

data(daxreturns)

# select the R-vine structure, families and parameters

# using only the first 4 variables and the first 250 observations

# we allow for the copula families: Gauss, t, Clayton, Gumbel, Frank and Joe

daxreturns <- daxreturns[1:250, 1:4]

RVM <- RVineStructureSelect(daxreturns, c(1:6), progress = TRUE)

#> ALV.DE + BAYN.DE --> ALV.DE,BAYN.DE ; BAS.DE

#> BAS.DE + BMW.DE --> BAS.DE,BMW.DE ; ALV.DE

#> BAYN.DE + BMW.DE --> BAYN.DE,BMW.DE ; ALV.DE,BAS.DE

## see the object's content or a summary

str(RVM)

#> List of 20

#> $ Matrix : num [1:4, 1:4] 3 4 1 2 0 2 4 1 0 0 ...

#> $ family : num [1:4, 1:4] 0 5 5 2 0 0 4 2 0 0 ...

#> $ par : num [1:4, 1:4] 0 1.183 1.111 0.648 0 ...

#> $ par2 : num [1:4, 1:4] 0 0 0 2.48 0 ...

#> $ names : chr [1:4] "ALV.DE" "BAS.DE" "BAYN.DE" "BMW.DE"

#> $ MaxMat : num [1:4, 1:4] 3 2 2 2 0 2 1 1 0 0 ...

#> $ CondDistr :List of 2

#> ..$ direct : logi [1:4, 1:4] FALSE TRUE TRUE TRUE FALSE FALSE ...

#> ..$ indirect: logi [1:4, 1:4] FALSE FALSE FALSE FALSE FALSE TRUE ...

#> $ type : chr "D-vine"

#> $ tau : num [1:4, 1:4] 0 0.129 0.122 0.449 0 ...

#> $ taildep :List of 2

#> ..$ upper: num [1:4, 1:4] 0 0 0 0.444 0 ...

#> ..$ lower: num [1:4, 1:4] 0 0 0 0.444 0 ...

#> $ beta : num [1:4, 1:4] 0 0.146 0.137 NA 0 ...

#> $ call : language RVineStructureSelect(data = daxreturns, familyset = c(1:6), progress = TRUE)

#> $ nobs : int 250

#> $ logLik : num 188

#> $ pair.logLik: num [1:4, 1:4] 0 3.84 3.76 71.62 0 ...

#> $ AIC : num -360

#> $ pair.AIC : num [1:4, 1:4] 0 -5.67 -5.52 -139.24 0 ...

#> $ BIC : num -332

#> $ pair.BIC : num [1:4, 1:4] 0 -2.15 -2 -132.2 0 ...

#> $ emptau : num [1:4, 1:4] 0 0.126 0.112 0.432 0 ...

#> - attr(*, "class")= chr "RVineMatrix"

summary(RVM)

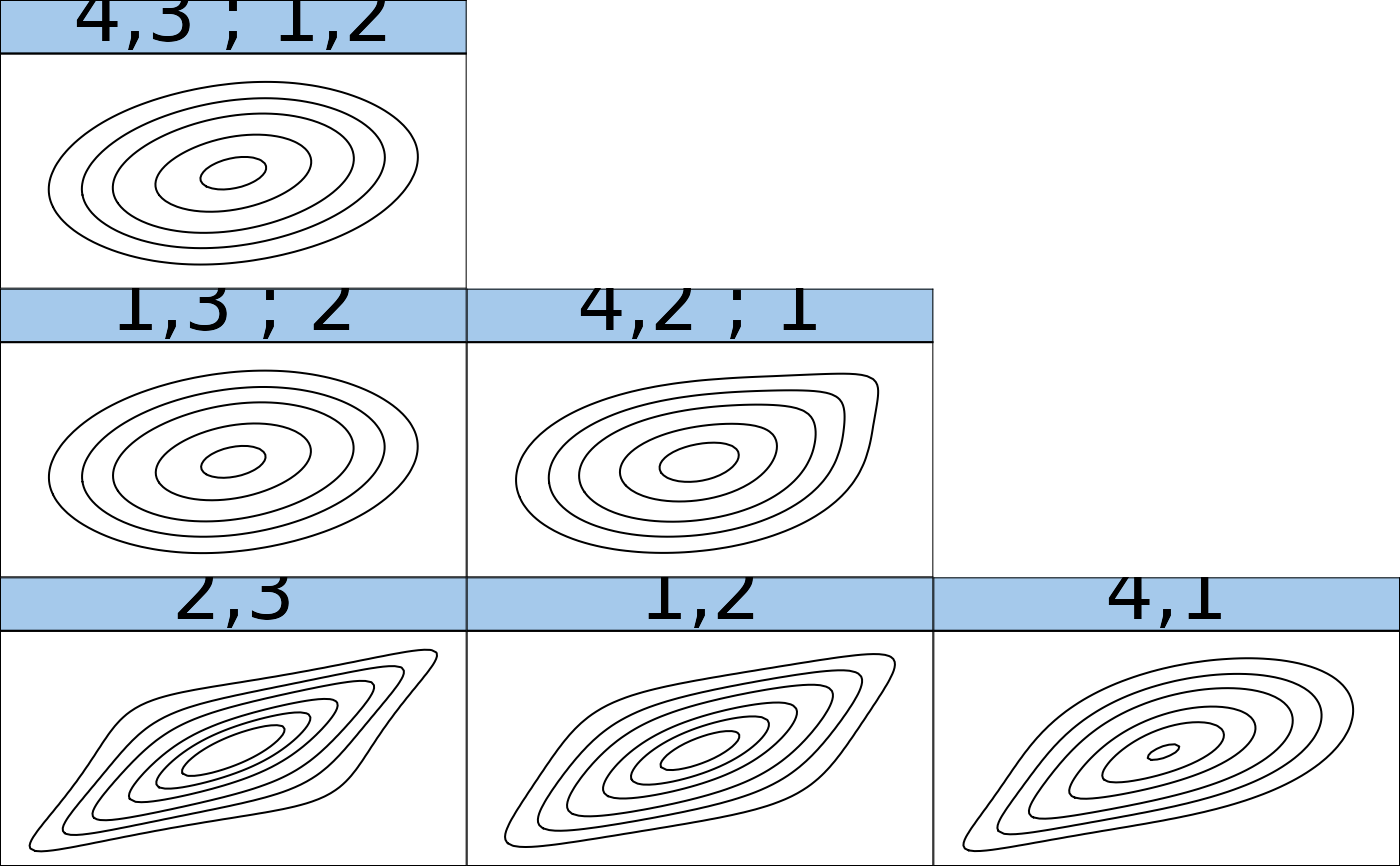

#> tree edge | family cop par par2 | tau utd ltd

#> ----------------------------------------------------------

#> 1 2,3 | 2 t 0.65 2.48 | 0.45 0.44 0.44

#> 1,2 | 2 t 0.61 3.55 | 0.42 0.35 0.35

#> 4,1 | 14 SG 1.62 0.00 | 0.38 - 0.46

#> 2 1,3;2 | 5 F 1.11 0.00 | 0.12 - -

#> 4,2;1 | 4 G 1.22 0.00 | 0.18 0.24 -

#> 3 4,3;1,2 | 5 F 1.18 0.00 | 0.13 - -

#> ---

#> type: D-vine logLik: 187.94 AIC: -359.87 BIC: -331.7

#> ---

#> 1 <-> ALV.DE, 2 <-> BAS.DE, 3 <-> BAYN.DE, 4 <-> BMW.DE

## inspect the fitted model using plots

if (FALSE) plot(RVM) # tree structure # \dontrun{}

contour(RVM) # contour plots of all pair-copulas

## estimate a C-vine copula model with only Clayton, Gumbel and Frank copulas

CVM <- RVineStructureSelect(daxreturns, c(3,4,5), "CVine")

## determine the order of the nodes in a D-vine using the package TSP

library(TSP)

d <- dim(daxreturns)[2]

M <- 1 - abs(TauMatrix(daxreturns))

hamilton <- insert_dummy(TSP(M), label = "cut")

sol <- solve_TSP(hamilton, method = "repetitive_nn")

order <- cut_tour(sol, "cut")

DVM <- D2RVine(order, family = rep(0,d*(d-1)/2), par = rep(0, d*(d-1)/2))

RVineCopSelect(daxreturns, c(1:6), DVM$Matrix)

#> D-vine copula with the following pair-copulas:

#> Tree 1:

#> 2,3 t (par = 0.65, par2 = 2.48, tau = 0.45)

#> 1,2 t (par = 0.61, par2 = 3.55, tau = 0.42)

#> 4,1 Survival Gumbel (par = 1.62, tau = 0.38)

#>

#> Tree 2:

#> 1,3;2 Frank (par = 1.11, tau = 0.12)

#> 4,2;1 Gumbel (par = 1.22, tau = 0.18)

#>

#> Tree 3:

#> 4,3;1,2 Frank (par = 1.18, tau = 0.13)

#>

#> ---

#> 1 <-> ALV.DE, 2 <-> BAS.DE, 3 <-> BAYN.DE,

#> 4 <-> BMW.DE

## estimate a C-vine copula model with only Clayton, Gumbel and Frank copulas

CVM <- RVineStructureSelect(daxreturns, c(3,4,5), "CVine")

## determine the order of the nodes in a D-vine using the package TSP

library(TSP)

d <- dim(daxreturns)[2]

M <- 1 - abs(TauMatrix(daxreturns))

hamilton <- insert_dummy(TSP(M), label = "cut")

sol <- solve_TSP(hamilton, method = "repetitive_nn")

order <- cut_tour(sol, "cut")

DVM <- D2RVine(order, family = rep(0,d*(d-1)/2), par = rep(0, d*(d-1)/2))

RVineCopSelect(daxreturns, c(1:6), DVM$Matrix)

#> D-vine copula with the following pair-copulas:

#> Tree 1:

#> 2,3 t (par = 0.65, par2 = 2.48, tau = 0.45)

#> 1,2 t (par = 0.61, par2 = 3.55, tau = 0.42)

#> 4,1 Survival Gumbel (par = 1.62, tau = 0.38)

#>

#> Tree 2:

#> 1,3;2 Frank (par = 1.11, tau = 0.12)

#> 4,2;1 Gumbel (par = 1.22, tau = 0.18)

#>

#> Tree 3:

#> 4,3;1,2 Frank (par = 1.18, tau = 0.13)

#>

#> ---

#> 1 <-> ALV.DE, 2 <-> BAS.DE, 3 <-> BAYN.DE,

#> 4 <-> BMW.DE